Daily Globe British Values, Global Perspective

Daily Globe British Values, Global Perspective

Related Articles

Remain economists predicted that a Leave vote in the referendum would produce an immediate meltdown of the UK economy. The meltdown was the expected result of voting Leave and the “uncertainty” this might cause. As George Osborne neatly summarized:

The predictions were explicitly for the period from the Referendum to actual Brexit (2016-2019). Predictions for after Brexit were for normal, or better than normal, growth (see below).

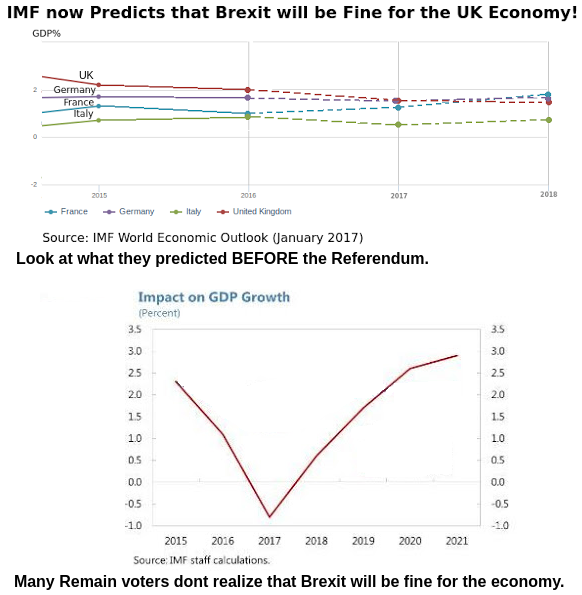

Consider the much publicised IMF predictions. The UK is adopting what the IMF labelled the “Adverse Scenario” but the IMF has now revised its predictions! Brexit will now be fine with GDP growth in the normal range for W.Europe:

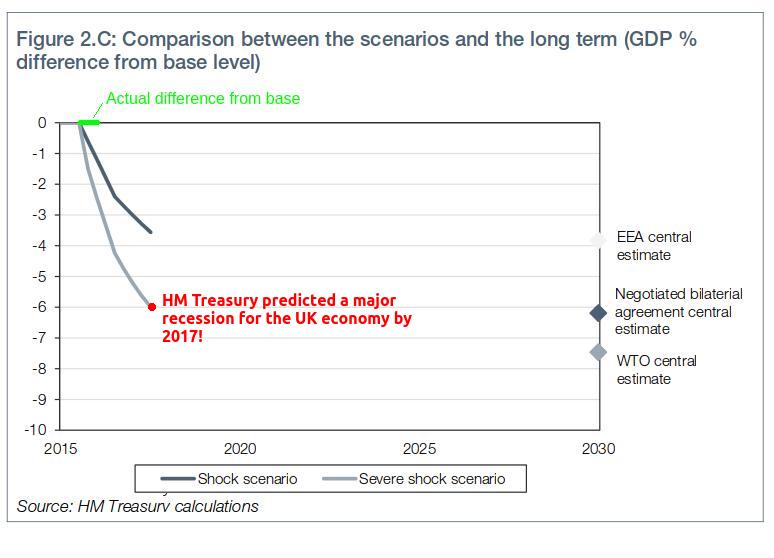

Look at what the Treasury predicted for 2017 before the Referendum – see HM Treasury Model :

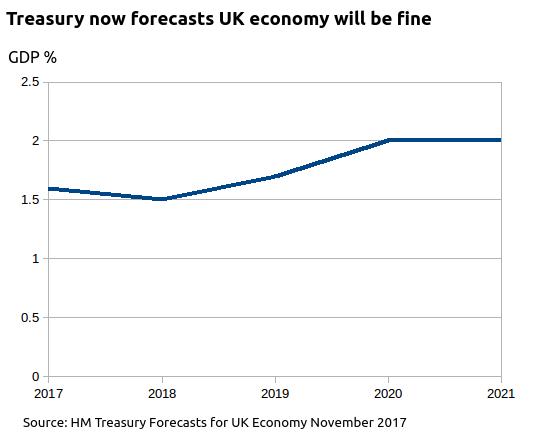

Fortunately the UK did not experience the worst recession for a century over the last year. The Treasury, under George Osborne were entirely wrong. The current Treasury predictionsare shown below:

The UK economy has been broadly following other advanced economies. There has been no catastrophic discontinuity as the “Experts” predicted (ie: “Remain Experts”).

The Bank of England has also utterly changed its position and predicts good growth compared with its Referendum predictions.

|

| Times: Britain has world’s top economy |

The Bank of England and the UK Treasury employ an army of economists, many of whom had communicated with the IMF about its predictions. Soon after the referendum the Bank of England forecast near recession growth of 0.1% for the UK economy for June to September 2016 (Q3). By September it was clear that this forecast was hopelessly wrong and growth was in reality strong at 0.5% for Q3 and 0.7% for Q$ bringing the UK to be tied with Germany for the fastest growing economy in the G7. Remain activists at the time attempted to argue that the predicted recession was avoided because Art 50 had not been invoked but as can be seen from the Bank of England position, the predictions were not based on invoking Article 50, they were based on “uncertainty” and were wrong, as the Bank has now freely admitted (see Times article above).

So, its official, all the Brexit gloom was indeed just scaremongering.

The key to the failure of the Remain economist’s forecasts is that they assumed that investment would fall drastically after the Referendum. This has not happened:

Investment in the UK has remained at near record highs since 2015. Obviously if you were uncertain about whether to invest you would have begun that uncertainty immediately after the Referendum.

The reporting of these predictions as highly probable, despite being based on the extremely shaky, untested foundations of “uncertainty” theory, was at best Fake News and at worst downright lying. The FT, Economist, BBC etc all had economics correspondents who knew that the predictions were extremely suspect.

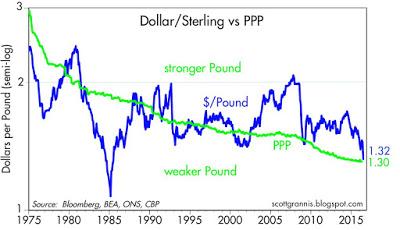

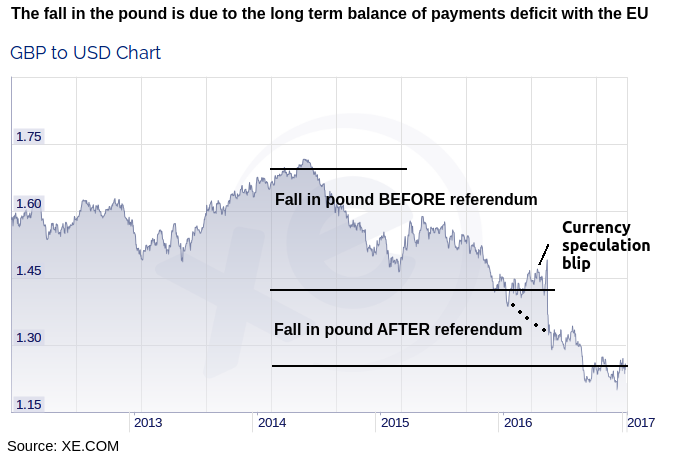

Nearly all of the economic data since the EU Referendum has been good. Retail sales are up, confidence has rapidly recovered after a brief fall, exports are up and imports are down. The fall in the pound has been excellent news, it was overvalued due to the flight of Euros from the unstable Eurozone and this has been corrected so that the pound is back to its real value:

|

| (Notice pound has been falling since 2014) |

The latest adjustment in the value of the pound after the referendum completes the move back to a realistic exchange rate that began in 2014. The Eurozone has become less financially unstable since 2014 and this has reduced the flight of Euros into Sterling. Had there not been a speculative blip upwards in the value of sterling before the referendum the current fall back to the PPP (Purchase Power Parity) value of the pound would have been unexceptional, the pound would just have been continuing its fall due to the Balance of Payments crisis.

The fall in the pound has been independent of any poor economic data except the Balance of Payments Current Account deficit and there was a flurry of speculation around the date of the Referendum.

The Bank of England confirmed that the Balance of Payments would cause the pound to fall: “A persistent current account deficit could lead to a sudden adjustment in capital flows or depreciation of the exchange rate, with adverse consequences for UK financial stability.” Bank of England.

The fall in the pound is not due to any poor economic performance after the Referendum – the UK economy has been performing very well since the Referendum, except for continuing Balance of Payments problems.

The reason that the IMF, PwC, Treasury etc. used “uncertainty” immediately after the referendum as their main argument against Brexit was that all of the experts, Remain or Leave, predicted good growth after Brexit actually happens. Here are quotes from their analyses:

“The UK economy then experiences faster growth in the medium term at 2.6% on average in 2021-25, before settling at around 2.4% per annum in 2026-2030.” PWC: Implications of an EU Exit

“Growth rates in later years are higher than the baseline..” IMF Country Report for UK

Much of the economic data since the EU Referendum has been good and even the Remain economists predicted it would be excellent after Brexit.

So, either Remain economists got the economics of Brexit totally wrong, or they were trying to scare the People into being obedient.

Not only have the Remain Broadcast Media, such as the BBC, failed to cover the shocking lies told by Remain economists, they are actively suppressing all data on the terrible trade and balance of payments deficits with the EU. The Broadcast Media have persuaded most Remain voters that they were cheated when the simple truth is that they were wrong. It is the Remain Broadcasters who are dividing the country.

There is much talk of “Brexit Lies” but the Remain campaign said that the Referendum would create a fall of about 3-5% in GDP and so cost an annual £75 bn to £125 billion a year (total GDP = £2 trillion).

The broadcasters have also covered the Leave suggestion of investing in the NHS the £350bn a week that they said could be saved by leaving the EU in 2019 as a “promise” that has already been broken. Despite the fact that Leave was not supported by any party that had a chance of government and was not able to make “promises” and it is not yet 2019.

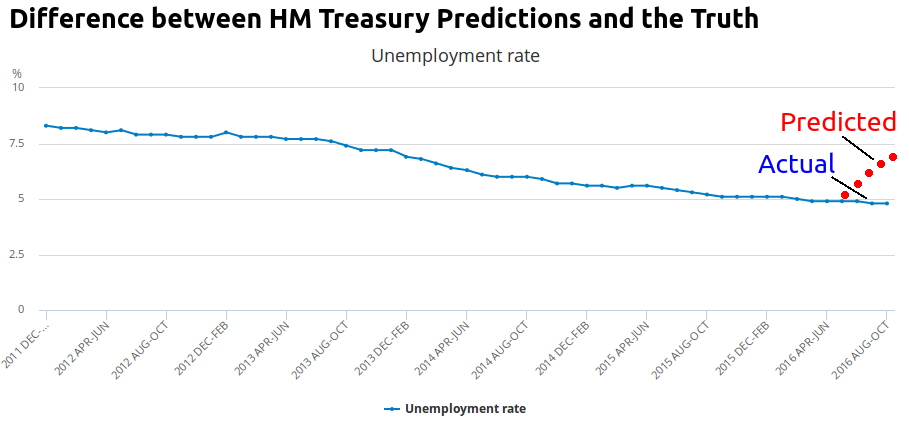

The worst “Experts” of all were the HM Treasury whose “dodgy dossier”, HM Treasury Analysis: The immediate impact of leaving the EU, should go down in history along with the Government’s Iraq War dossiers:

|

| HM Treasury Model predictions vs ONS Data for Unemployment |

|

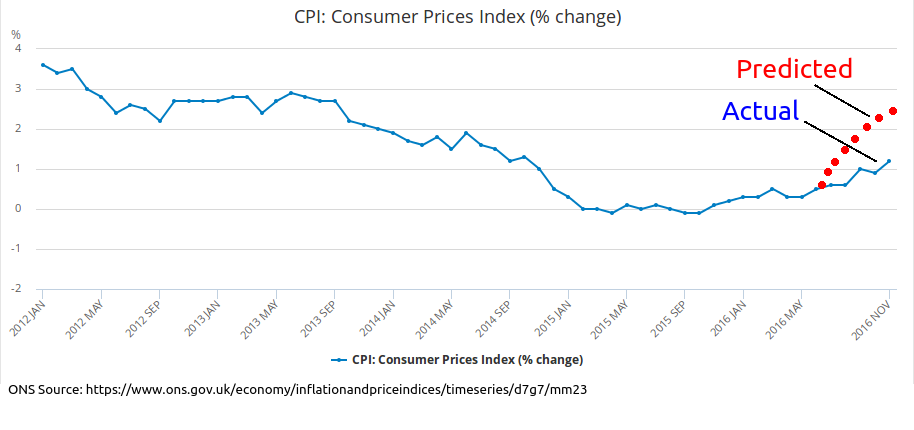

| ONS CPI Data |

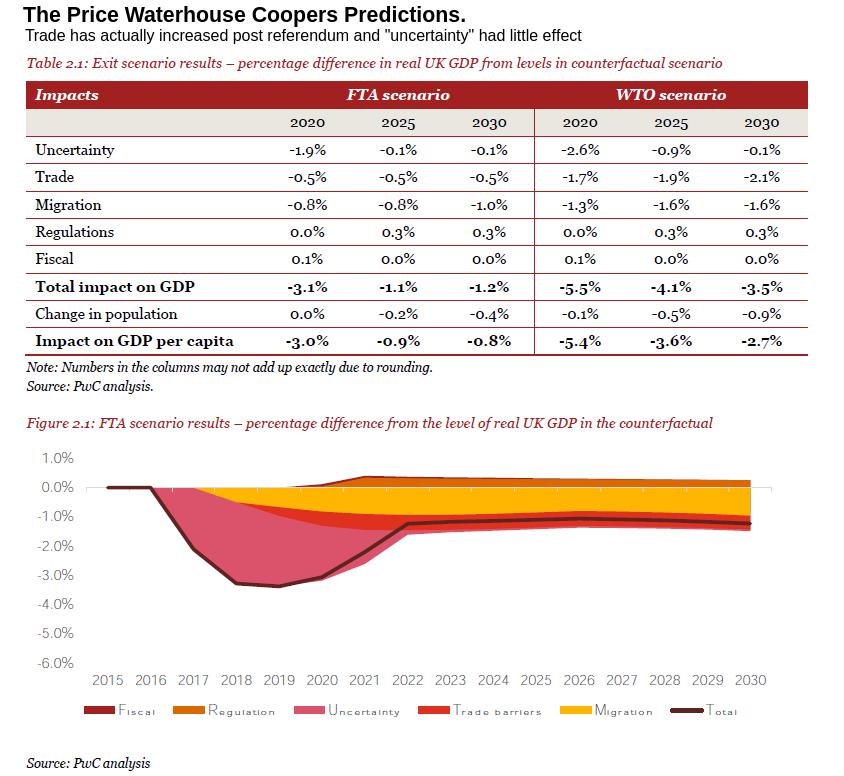

Many other Remain pundits repeated the IMF mistake. Price Waterhouse Coopers predicted a massive meltdown after the Referendum, due to “uncertainty”, that has not happened:

|

| PWC: Implications of an EU Exit |

The PwC graph above is extremely sneaky. The data points are predicted cumulative effects so the recovery from 2019 to 2022 is actually due to strong growth happening after Brexit occurs (IMF had same prediction – see above)!

The BBC and other Remain campaigners are now routinely blaming any adverse or apparently adverse data on Brexit. For instance inflation is being blamed on Brexit even though it is being experienced in many developed economies that are avoiding deflationary pressures:

This post was originally published by the author on his personal blog: http://pol-check.blogspot.com/2017/02/remain-predictions-for-brexit.html

{kind=link}